Derivatives & Futures

by PRASHANT SHAH -

Derivatives

Derivative is a market segment of trading. In India, there are two major stock exchanges – National Stock Exchange or NSE and Bombay Stock Exchange or BSE where people can buy and sell shares. That segment is known as cash or the spot segment.

There is separate segment called the derivative segment at NSE & BSE. NSE Currency and MCX Commodity segments are other derivative markets in India. Derivatives a leveraged instrument where in you can take a position by paying a margin.

There are two types of instruments in derivative segments:

Futures and Options.

Both these instruments are very useful and offer interesting opportunities from a trading perspective. They are very useful if you understand the concepts and fundamental principles of using it.

I shall try to explain these instruments and more about trading Options right from very basics in a simple language while remaining to the point.

Before we discuss Options strategies in detail, we need to understand basics of Options. And before that, we need to understand Futures.

Futures Segment

When we trade shares in the cash segment, we can easily trade the quantities of our choice. In the derivative segment we don’t trade shares, we trade fixed-size contract of the chosen share.

Not every stock that is trading in the cash segment is listed in the derivative segment. Derivative segment is also known as F&O (Futures and Options) segment. Currently, there are 200 stocks available in the F&O segment. Exchanges keep adding and removing the stocks from this list based on the pre-defined criteria.

Unlike cash segment, traders don’t trade shares in the derivative segment. They enter into a contract. There is a contract between a buyer and the seller every time they make a transaction. But you don’t have to sign the contract every time while making the transaction. The terms of the contract are fixed and you agree to it when you make the transaction.

In the derivative segment, the quantities are fixed. It is known as a ‘lot’. These quantities vary for different stocks and it is decided by the exchange. Each stock has a fixed quantity which is known as a lot size. When you buy 1 lot you buy minimum quantity which is the lot size of that instrument.

For example, there is a stock called SSK listed in Cash as well as derivative segment.

For example, SSK is trading at ₹100/- in the cash segment. I want to buy 500 shares of it. I will have to pay ₹50,000 to buy it. This will be a transaction in the cash segment.

Let’s assume that the lot size of the SSK in derivative segment is 500 shares. That means I will have to buy a minimum of 1-lot instead of buying the 500 shares.

When lot size is 500, you have to buy minimum 500 shares i.e 1 lot. You can’t buy fraction of it. You can’t buy less than 1 lot so the minimum quantity you can buy is 500 shares. You can only buy the quantities in multiples of the lot size. So, when you buy 1 lot you buy 500 shares. When you buy 2 lots you buy 1000 shares and so on.

If the lot size is 200 shares, you buy 200 shares when you buy 1 lot. You buy 400 shares when you buy 2 lots and so on.

So, if lot size of SSK is 500 and someone tells you that he has 5 lots of SSK, that means he has got 2500 shares of SSK. He has got 5 contracts of SSK having 500 quantities each.

Margin

Now question will be, why should I buy it in derivative segment. I can buy 500 shares of SSK in cash segment as well.

In the cash segment, you will have to pay ₹50,000 to buy the 500 shares of SSK. When you a buy a future contract of SSK, you don’t have to pay full amount required to buy those shares. You have to pay just the margin amount decided by the Exchange. Let’s say margin is 20% of the contract value.

The contract value is ₹50,000 (100 x 500)

20% Margin is ₹10,000 (20% of 50000)

So, by paying 10,000 as margin amount, you can buy 1 lot (500 shares) of SSK in the derivative segment.

The margin is blocked when you trade in Futures. It includes SPAN margin and exposure margin. SPAN margin is the minimum prescribed margin that is blocked based on the exchange's instructions when you create a derivative position. In order to mitigate any MTM losses, exposure margins are blocked over and above SPAN margins. SPAN and exposure margins are determined by the exchange. Based on certain parameters, this total margin changes frequently. Stock exchanges update it throughout the day as well.

So, if margin of the stock is 20%, the lot size is 500 and the price of the instrument is ₹150.

You will have to pay ₹75,000 margin to purchase 5 lots (2500 qty) of the stock instead of paying ₹375000/-.

If you get that, you have understood the concept.

We discussed about Lot size and Margin of Futures. These are the commonly used terms while you trade in derivative contract.

Long-Short

Another feature of derivative trading is that unlike cash segment, you can also sell the stocks even if you don’t own it.

We buy shares when we feel company is doing well and expect the share to rise. We exit the trade when we think that the stock will not go up now. But what if we think share will go down from here? We cannot sell the shares that we don’t own in cash segment. But, in the derivative segment, you can sell the contract if you think the price will go down. It is known as Shorting.

When someone buys a contract, there is someone who sells it. It is not necessary that a person selling it is having that quantities in his portfolio. It’s a contract, not share. So, you can sell the contract even without having the buy position of the contract.

- When you buy the contract, it is known as Long.

- When you exit your buy position, it is known as Long exit.

- When you sell the contract, it is known as Short selling.

- When you exit you short position, it is known as Short covering.

So, you can also sell the 5 lots of SSK by paying the span margin amount (₹75000/-) if you think the price of SSK will fall.

Expiry

The contracts in the derivatives segment have an expiry date. Unlike shares, you can’t hold them for as long as you wish.

In India, the expiry of most NSE derivative segment happens on the last Thursday of every month.

So, if you buy any contract, it will expire on the last Thursday of the month. You must exit your trade before it expires.

So, if you have a long position in 1-lot of SSK, you will have to exit it before the expiry (last Thursday of the month). If you have a short position of SSK 1-lot, you will have to exit or cover it before the expiry (last Thursday of the month). If you do not cover the position, the futures contract will expire, and the position will be closed on the last Thursday of the month or the expiration date.

Apart from stocks, the indices like Nifty and Bank Nifty are also traded in the derivative segment. This is another advantage of this segment; you can easily buy or even short the index.

If you want to buy Nifty basket in the cash segment, you will have to buy all 50 stocks of Nifty and maintain that which will be a tedious task.

Instead of that, you can buy Nifty future contract in the derivative segment. You will have to pay less margin and you don’t have to worry about rebalancing individual stocks based on the weightage. If Nifty goes up, Nifty futures price will also go up. You can even short the Nifty or Bank Nifty index if your view is bearish.

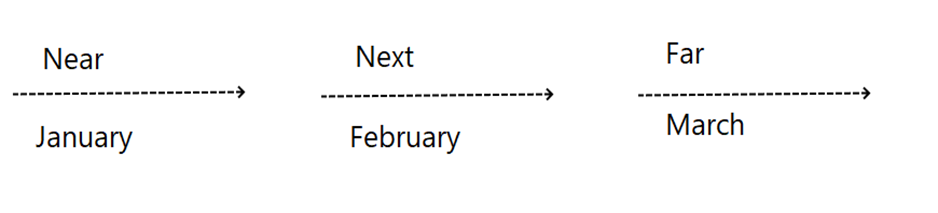

There are three expiry contracts that are traded at any given time. Current month expiry is known as a ‘Near’ month contract. The last Thursday of the current month is known as Near month expiry and the contract is known as near month contract.

For example, if the current month is January, then the last Thursday of January is the near-month expiry date. January month contract would be called as the near month contract.

February month contract would qualify as the Next month contract.

March month contract would be known as Far month contract.

When January contracts expire on last Thursday of January, February contracts becomes the Near month contract. The March month contracts become Next month contract and the April contracts become Far month contracts.

This cycle keeps repeating. Essentially, there will be three contracts open at a time for any instrument and each contract will have a three-month life.

So, when you want to buy 1 lot of SSK stock you will have three options: buying Near month contract, buying Next month contract, or buying Far month contract.

If current month expiry (Last Thursday) is near, you might want to buy the next month contract.

Exercise

If you don’t close the contract before the expiry day, it gets squared off by the exchange when the market closes. Remember, the expiry day is usually the last Thursday of the current month. All open contracts get settled at the expiry price of each instrument. Expiry price is the average price of last 30 mins of the trading on the expiry day.

For example, if you buy SSK contract at ₹100 and did nothing till the expiry day and let us assume that the expiry price happens to be ₹98. Your contract will get closed on that day and transaction will be settled at ₹98.

Roll-over

Futures contract will expire on Thursday and there is no choice. People usually roll over the contracts if they want to carry the position for beyond the current contract expiry. In such a case they will have to roll over the contract.

Roll over is a simple concept.

Suppose you have a long position of SSK Future contract of Near month expiry.

If you wish to remain long in SSK future beyond the expiry period of the current contract, you can exit the Near month contract and buy the next month contract of SSK future.

This switchover from one contract to the next one is known as a long position roll over of the contract. You will get back the margin you paid for the near month expiry, and you will have to pay margin for the next month expiry.

In the process, there is a possibility that you may incur some cost.

For example, you bought SSK future contract of near month at ₹100. You exited it at ₹98 before the near month expiry day and bought next month contract of SSK at ₹99 because it was trading at that price.

This roll over transaction resulted in a ₹1 extra cost apart from brokerage and taxes. This is the cost you paid to roll over and carry your long position in the contract.

Similarly, if you have a short position of SSK Future contract of Near month expiry. You cover the Near month contract and short the next month contract of SSK future.

This is known as a short position roll over of the contract. People also do it on the last day of expiry but often the cost of the roll over is high on that day. Usually, the roll over cost is high during last week of the expiry.

Truly speaking, it is nothing but settling the current month contract and creating the same position in the next month contract.

Premium – discount

Imagine, SSK share is listed in cash segment and derivative segment as well. There are three contracts in derivative segments. All these are being traded simultaneously.

The underlying instrument is SSK in cash segment. If the price rises, the future contracts will also rise. If the value of the underlying instrument goes down, the SSK price in future segment will also fall.

But because they are trading separately, there can be difference in the price of the cash segment and the derivative segment.

- When the price of derivative segment is higher than the price of the cash segment, it is said that the futures price is trading at a premium.

- When the price of derivative segment is trading at price lower than the cash price, it is said that the futures price is trading at discount.

If SSK stock price is 100 in cash segment and 110 in derivative segment, it is trading at a ₹10 premium.

If SSK stock price is 100 in the cash segment and 90 in the derivative segment, it is trading at ₹10 discount.

All contracts can have different premiums and discounts. Usually, derivative contracts trade at a premium. When they trade in discount, it is considered as a bearish sign.

There can be multiple reasons for the premium or discount. For example, in case the company declares dividend, the future contract holders are not entitled to the dividend. So, there can be a difference between price in cash and futures segment when the dividend is declared, and the price is quoted cum-dividend in the cash market.

So, you must study the reason when you see premium or discount in derivative segment for any instrument.

MTM

When you buy a share, you make a profit or loss when you sell it.

For example, you bought a stock at 100, it fell to 90. Your portfolio value drops but it is a notional loss because you have not exited the stock yet. If you sell it when it rises to 120, you made a profit of ₹20 per share.

In the derivative segment for Futures, the profit or loss is booked at the end of every market day.

If you bought a contract at 100 and if it falls to 90, you will have to pay the difference amount of ₹10.

Suppose on the next day, if price goes to 105, you will get the credit of ₹15 (105 – 90).

This is known as Market-to-Market (MTM). You pay lesser margin when you buy Future, but you will have to pay the MTM loss on a daily basis if the price does not move in your favor.

Investment

Your investment when you buy a future contract is the margin of the contract, but you will also have to make some arrangement for the potential MTM losses too.

Many people don’t understand this important aspect. Even though you can trade in the contract at lesser amount (span margin), you have to keep funds for MTM loss that gets calculated on daily basis.

Arbitrage and Hedge

Some traders also use derivatives for arbitrage.

For example, you bought SSK company 500 shares in cash at ₹100 and sold 1 lot (500 qty) in future at ₹99, you gain ₹1 difference. This is known as arbitrage. However, this arbitrage trading is not advisable for retail traders as the returns are often meagre. One has to trade big size in order to make any meaningful profits in such arbitrage trades.

There is also a concept called Hedge.

For example, you have a large amount of stocks in your portfolio. You are worried that market will go down and in the process your portfolio value could take a hit. In such a scenario, you can short couple of lots of Nifty to protect the potential damage to your portfolio.

If market gaps down or falls suddenly, your portfolio stocks will fall but you can limit your loss and make money in your short position in Nifty.

Going short in Nifty to mitigate the loss in value of your portfolio is a simple example of hedge.

We will discuss more about hedge positions after the discussion on Options. Let’s discuss Options instrument.

I hope you are clear about how Future contract works.

People typically trade in Futures based either on technical analysis or fundamental analysis or any other method of analysis. They form their view based on their studies and take positions in the derivatives market.